Both law enforcement and the District Attorney's Office are fully committed to catching those who fraudulently pass bad checks and prosecuting them to the fullest extent of the law.

When we prosecute the case, the case is only as good as the evidence that can be collected. Much of that evidence only is available if you have secured it from the person that wrote the check.

We urge you to become our partners in eliminating check fraud by following the steps outlined here for the checking identification and signatures. Hopefully just following these steps will put a dent in fraudulent checks, but where they still occur, you'll have the evidence that allows us to catch and prosecute the offender.

Kala Beauvais, District Attorney

Please print and fill out this form.

The following tips are suggestions to help you establish good procedures for accepting checks.

-

Institute a check acceptance policy.

A clearly posted check acceptance policy for your employees and customers can go a long way toward reducing your losses. Policies should state which types of checks can and cannot be accepted and include the consequences to bad check writers.

-

Confirm the identity of the check writer.

All I.D. can be forged. The most reliable form of I.D. is that which contains a photo and a physical description. Take the I.D. in hand and write the I.D. number, birth date, address and other descriptive data on the front of the check. Have check writers give an inked fingerprint impression on the check. Have employee initial and date the check at the time of acceptance. Have backups where possible - copies of I.D., I.D. by a second employee, security camera or video. Trust your instincts! If something doesn't seem right, ask questions or ask for another form of payment. You are not obligated to accept a check.

-

Whenever possible, avoid accepting checks written on a new account.

Approximately 85 percent of all bad checks are written on accounts only a few months old and reflect check numbers between 101 and 150. Use caution. Do not accept counter drafts.

-

The signature should be legible and signed in the presence of the individual accepting the check.

Do NOT accept previously signed checks. For a company check, it is vital that the signature is legible. If not, print the individual's name on the front of the check.

-

The complete address should be imprinted on the check.

Require a street address, in addition to a P.O. Box number. Obtain a phone number as well.

-

Inked fingerprints.

Businesses that utilize the inked fingerprint method provide convincing, reliable evidence of the identity of the person passing the check or attempting to misrepresent his or her identity.

-

Accept checks only written with today's date.

Pre- or post-dated checks are NOT accepted in the Bad Check Restitution Program and CANNOT be criminally prosecuted. This restricts any recourse, you may have against the check writer if your own collection attempts fail.

-

Make sure written amounts and number correspond.

Banks will NOT honor checks with discrepancies between written amounts and numbers.

-

Avoid accepting checks drawn on an out-of-state bank.

REMEMBER: You are NOT required to accept a check from anyone. If you feel uncomfortable or suspicious, trust your intuition! Ask for another form of payment.

-

Obtain proper I.D.

-

Using the right index finger, have the person touch the ink pad and then touch their finger on the bottom center of the check, above the account number. Keep the print clear of the account number to prevent misreads of the account number at the bank clearing house. (See example below.)

-

Firmly press finger on document. DO NOT ROLL OR SLIDE FINGER. Note: In some cases a person may not have a right index finger. If this happens, ask them to use a different finger, and then note on the check which finger is used.

-

Make sure print is clear and readable.

-

Have the person rub their fingers together to remove any residue.

-

DO NOT accept pre-fingerprinted checks.

Touch ID Pads can be obtained through several different vendors.

Three Steps to File a Check Fraud Report

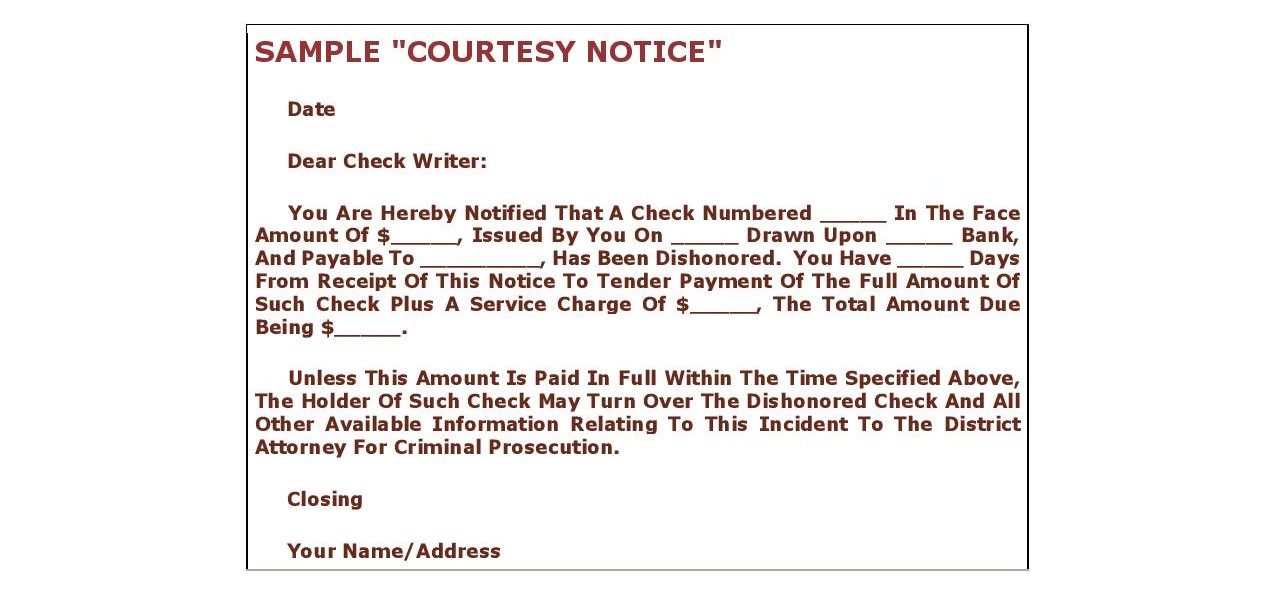

1. Make personal contact with the check writer. If that is unsuccessful, send a courtesy notice, certified return receipt, stating the check writer has 15 days to respond and remit payment.

2. If you do not hear from the check writer or receive payment, click on "form download" (see above) for a printable Bad Check Crime Report form.

3. Fill out the Crime Report form, attach originals or legal copies (you retain photo copies) of all checks (front and back of checks) and notification documents, such as return receipts and bank notices, and mail to:

Tenth Judicial District Attorney's Office

ATTN: Check Fraud Unit

701 Court Street

Pueblo, CO 81003

Once a report has been filed, DO NOT ACCEPT PAYMENT DIRECTLY FROM THE CHECK WRITER. Restitution payments must be coordinated by the District Attorney's Office. Should the check writer contact you to make payment, direct them to the District Attorney's Office Check Fraud Unit at 719-583-6030.

A check is "eligible" if:

- There is no minimum dollar restrictions.

- A photo I.D. (drivers license, military I.D., state I.D. card) was recorded at the time of the transaction.

- It was received in Pueblo County, deposited into a bank in exchange for goods or services and presumed "good" at the time of acceptance.

- A "Courtesy Notice" was sent to check writer allowing 15 days to make good on the check.

A check is "ineligible" if:

- It is returned from the bank stamped "Account Closed" or "Unable to locate". (Report directly to the Pueblo Police Department or Pueblo County Sheriff Office.

- It is stolen or counterfeit. (Report directly to the Pueblo Police Department or Pueblo County Sheriff Office.

- It is post-dated.)

- Both parties knew there was insufficient funds at the time of the transaction.

- It is a two-party, government issued, payroll or travelers check.

- The identity of the check writer is unknown.

- There is no amount, date or signature on the check.

- It has not been processed by the bank.

- It is an ACH type payment.

- It is returned stamped "Stop Payment".

Checks ineligible for the Tenth Judicial District Attorney's Office Restitution Program may be pursued via small claims court process or by a private collection agency of your choice.